Photographs: Uttam Ghosh/Rediff.com Priya Nair, Yogini Joglekar

If you are looking to purchase a life insurance policy, do it before this October -- else you'll have to wait till 2013.

Reason: In its draft guidelines, the Insurance Regulatory and Development Authority (Irda) has asked the country's life insurance companies to refile their existing products and withdraw the same by September 30.

Irda takes around five to six months to clear a product, say industry players.

...

New life insurance policies might be worth the wait

Photographs: Uttam Ghosh/Rediff.com

There is good chance of the guidelines being finalised. From the customers' point of view, it may not be a bad idea to wait as the changes suggested will be more beneficial to customers, say experts.

These guidelines are designed to help promote the concept of insurance for protection rather than using it as an investment tool.

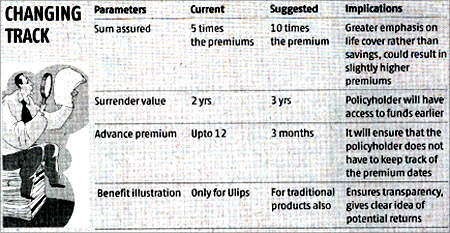

The greater emphasis on the life cover than savings will result in a higher sum assured. The minimum sum assured for all life insurance products except pension plans should be at least 10 times the premium, higher from the current norm of five times.

Otherwise, the premium paid will not be eligible for tax benefits under Section 80C. The 2012-13 Union Budget had prescribed this, following which the regulator mandated it in the draft.

...

New life insurance policies might be worth the wait

Photographs: Dominic Xavier/Rediff.com

"Since there will be an increase in the sum assured, there will obviously be a rise in the premiums, although it's difficult to predict the quantum," says Deepak Sood, managing director (MD) and chief executive officer (CEO) of Future Generali Life Insurance.

Then, the period after which a policy's guaranteed surrender value (GSV) can kick in, has been reduced for policies of less than 10 years.

Earlier, the guaranteed surrender value (the amount the customer is entitled to at the time of surrendering the policy) would kick in after three years for all traditional policies.

...

New life insurance policies might be worth the wait

Photographs: Uttam Ghosh/Rediff.com

But, the proposed norms suggest that products with a term of less than 10 years can be surrendered and GSV can be paid from the second year itself.

With this, the insured will now have access to his funds earlier than what he did. The lock-in period for Ulips continue to remain five years.

Many insurers collect advance premiums for up to 12 months. But the new norms restrict the advance premium payment to three months and that too, only on the date of commencement of policy or monthly policy anniversary. This will be applicable only for those who pay their premiums on a monthly basis.

...

New life insurance policies might be worth the wait

Photographs: Uttam Ghosh/Rediff.com

Suresh Agarwal, executive vice-president at Kotak Mahindra Life Insurance, says collecting premiums in advance is not conducive for customers.

"Collecting a lump sum in advance defeats the purpose of accumulating funds and habituating the person to save and plan in a disciplined way," he says.

In order to bring transparency, the regulator insists that all insurance products should provide the prospective policyholder a customised benefit disclosure (illustration) on guaranteed and non-guaranteed benefits for all products. Currently, this is mandatory only for Ulips.

...

New life insurance policies might be worth the wait

Photographs: Uttam Ghosh/Rediff.com

This benefit illustration should be signed by the customer and the agent which is part of the policy contract. This will give policyholders a clear idea of the returns they can expect.

The guidelines also call for rationalising agent commissions. Insurers, which pay high commissions to agents, in turn charge it to the customers by way of higher premia. Lower commissions will mean lower premia for customers.

"The overall standardisation as proposed in the guidelines, with regard to the minimum sum assured and surrender value, is good for customers," says P Nandagopal, MD and CEO, IndiaFirst Life Insurance.

...

New life insurance policies might be worth the wait

Photographs: Rediff Archives

These norms may help do away with complex products like NAV (net asset value) guaranteed products.

"Customers fail to understand that such products operate at a fund level and hence do not understand the actual implications of investing in them. NAV guaranteed products do not give maximising returns," he says.

article